Obama Department of Labor is finalizing a new regulation that would shut down anyone who offers any but the most generic financial advice. Like so much of the truly evil stuff the administration has done or tried to do, it is couched in terms of nannying independent adults because, you know, without a federal agency to help us out we are without hope.

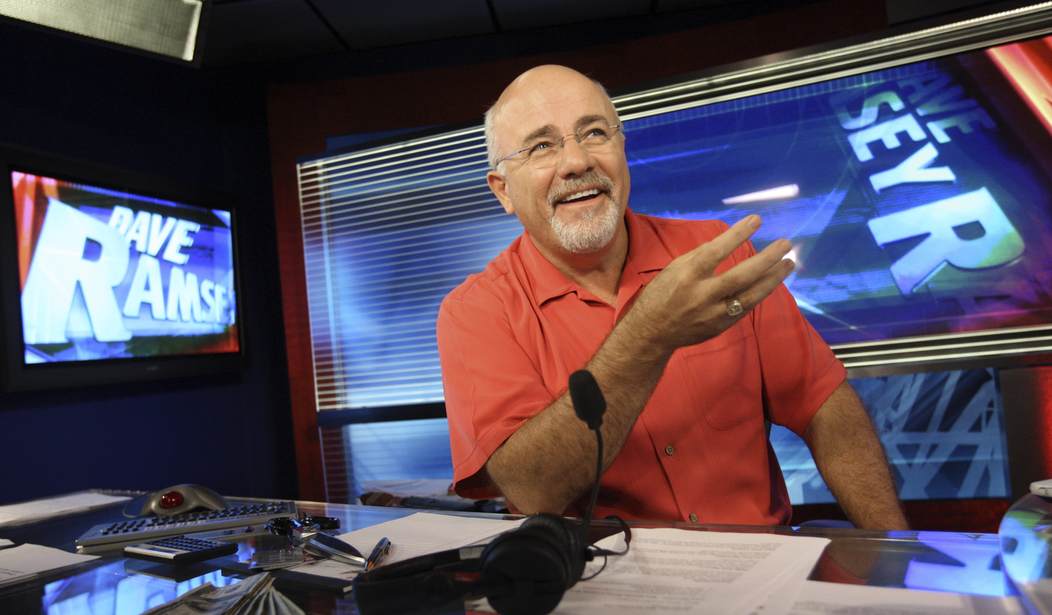

Experts both for and against the rule I have talked to agree its broad reach could extend to financial media personalities who offer tips to individual audience members, a group that includes not just Ramsey but TV hosts like Suze Orman and Jim Cramer, as well as many other broadcasters who opine on business and investment matters. They would be ensnared by the rule’s broad redefinition of a vast swath of financial professionals as “fiduciaries” and its mandate that these “fiduciaries” only serve the “best interest” of IRA and 401(k) holders.

The main focus of the Labor Department rule has been its likely effects on brokers and their customers. The rule creates a presumption against brokers taking third-party commissions from mutual funds they sell to savers. Because of this, savers who currently pay only a small commission on the execution of an order may have to pay a much larger fee based on a percentage of their assets, which would drive some brokers to simply stop serving middle-income investors. As I note in a new report for the Competitive Enterprise Institute, similar restrictions in Great Britain have caused a “guidance gap” in which brokers have largely stopped serving brokers with assets less than £150,000 ($240,000).

But the potential chilling effect of this rule on free financial discussion in the media is even more frightening. Kent Mason, a partner at the law firm Davis & Harman who has testified before Congress on the ill effects of the fiduciary rule, strongly disagrees with Markey that Ramsey and others should be shut up. But, worryingly, he says Markey is mostly right in his interpretation of the fiduciary rule’s ability to muzzle financial personalities.

“Under the proposed regulation, investment advice from a radio host to a caller regarding the caller’s own investment issues would appear to be fiduciary advice if the advice addresses specific investments,” Mason said in an email. It doesn’t matter that Ramsey and other hosts aren’t compensated by listeners, he adds, as the DOL rule explicitly covers those who give investment advice and receive compensation “from any source.” Mason agrees with Markey that the compensation Ramsey receives from radio stations that carry his show and from book sales are enough to define Ramsey as a “fiduciary” under the rule.

There are two parts to this assault on America. First, this is rent-seeking on the part of various financial interests. What they want is to be gatekeepers for all financial information and as part of that gatekeeping they want to be paid. Fair enough. But this is the classic use of the coercive power of the federal government in order to create a lucrative income for a service that is of really marginal value to the vast majority of people who would be forced to use it. Think of this as ObamaCare for your savings.

The second part is even more hideous. The idea that Dave Ramsey or Suze Orman are “financial advisors” with a fiduciary relationship to random callers is just crazy. The rule doesn’t hit just the big names. It hits local newspaper columnists who talk about financial subjects. It would, in its current form, apply to someone teaching a community college course on personal finance and offering solutions to problems posed by students.

This is not alarmism. The industry proponents of the regulation are crowing about it:

Ramsey Tweeted, “this Obama rule will kill the Middle Class and below ability to access personal advice.” A war of Tweets then broke out between opponents of the rule, and supporters, the latter of which includes fee-based investment advisers expected to benefit from the new costs the rule will shower on their broker competitors.

Fittingly, even before Ramsey came out against the rule, one of his critics called for using the rule against Ramsey, supposedly for providing advice said critic deemed harmful to savers. In an October article in LifeHealthPro, an online trade journal for insurance agents and financial advisers, Michael Markey, an insurance agent and owner of Legacy Financial Network, called for Ramsey to “be regulated and to be held accountable” by the government for the opinions he gives to listeners. Markey hailed the Labor Department rule as ushering a new era in which “entertainers like Dave Ramsey can no longer evade the pursuit of regulatory oversight.”

Congress is trying to act to stop the rule but this Congress has shown no inclination at all to fight Obama on anything in an election year, presumably because having your party stand for something in an election year is a bad idea in GOP circles. Ultimately, this rule is going to end up in court and it is hard to see how it survives the obvious constitutional challenges. But with a liberal majority on the US Supreme Court and a Chief Justice who seems devoted to supporting the administration any way he can, I’m not counting on the rule of law winning this encounter.

Join the conversation as a VIP Member