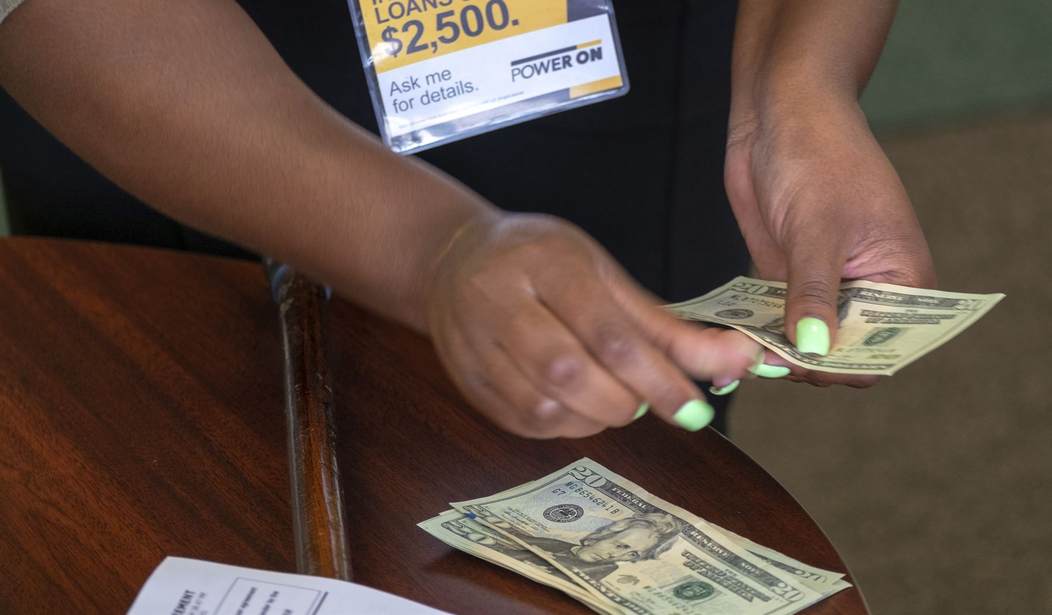

In this Aug. 9, 2018, photo a manager of a financial services store in Ballwin, Mo., counts cash being paid to a client as part of a loan. The firm offers cash-based financial services, including payday loans, installment loans, fund transfers and other financial services. The Consumer Financial Protection Bureau will revisit a crucial part of the bureau’s year-old payday lending industry regulations, the bureau announced Friday, Oct. 26. (AP Photo/Sid Hastings)

Last week the House Financial Services Committee held a hearing on fintech-bank partnerships. This hearing followed the introduction of a new California bill that went into effect on January 1st which limits the ability of the state’s financial industry to provide short term loans to consumers in need of emergency financial services.

I’ve written about it at length over the last year but to summarize, California’s AB539 caps installment loan between $2,500 and $10,000 at 36% in the hopes of “protecting” low-income loan consumers from paying exorbitant interest rates. In reality, the bill has done what other bills passed in the same legislative session have done: it has reduced financial options for people who need them most while severely undercutting a vital business-consumer relationship and driving some businesses and services out of state.

In short, it’s a loser for families who don’t meet the prime credit threshold, but there is still good news out there when it comes to lending. Options are available, thanks to bank lending that is supported by third party service providers.

In recent years, we’ve begun to see banks partner with the fintech industry to deliver financial products that serve a diverse customer base that has typically been frozen out of the credit market. Federal regulators have been very supportive of these partnerships, because they combine the ease and accuracy of modern technology with the financial strength and regulatory oversight of an established banking system.

Some politicians have argued against these partnerships, but they don’t understand this model and the opportunity it provides for people who are poorly served by the traditional financial market.

The HFSC hearing on fintech-bank partnerships highlighted the legitimacy of these partnerships and the important role they play in expanding access to highly regulated credit to Americans with nonprime credit scores. Banks partnering with third party vendors is nothing new. They have a long, established history in areas like mortgages. As the lender, the bank exercises ownership, discretion and control. The OCC and FDIC have strong third party guidance requiring the bank to manage conduct of its partner and hold it accountable. In addition, the partner is subject to examination by the bank regulator.

These true partnerships result in better underwriting on the front end and better servicing on the back end.

The financial tech industry (fintech) has expanded the economy and particularly our buying power in ways no one could have ever predicted. More importantly, iIt’s leveled the playing field for an entire subsection of American society.

Most fintechs use complex algorithms to calculate credit scores and leverage alternative data sources and machine learning to provide a more accurate picture of an applicant. Additionally, these companies build their products for online and mobile audiences, which makes the customer experience and access to services much easier and more transparent.

Banks have access to capital and an existing base of customers: the two biggest costs of doing business for a fintech company. When the cost of doing business is lowered, it can change the business model, allowing these companies in partnership with FDIC-chartered banks to lend to nonprime consumers at lower rates.

Fintechs find new ways to rate customers — ways that look beyond the sometimes outdated models of credit bureaus. FDIC-chartered banks have the capital and the insurance backing. It’s a modern match that benefits both the financial industry and the people who need it the most. A win-win.

Technology has been an incredible equalizer for the free markets. Even as states like California crack down on the freedom to conduct business when and where one pleases, credit consumers have the satisfaction of knowing that there are still many wonderful financial options available.

Limiting the options of free citizens is never true protection. The partnering of banks and fintechs can offer financial consumers more opportunities to remain in control of their own affairs and agreements while creating and fostering a healthy lending environment that works for everyone regardless of their credit status. The willingness (so far) of federal regulators to allow those relationships to thrive is a justice for nonprime borrowers. Let’s hope it stays that way.

Join the conversation as a VIP Member